What is Contract Works Insurance?

When you’re working on a construction site, plenty of things can go wrong. Damage or loss to a building could cost your time, money and even your reputation. Meanwhile, an onsite injury can result in considerable pain, stress and financial loss.

That’s why having the right amount and type of contract works insurance is an important part of your business toolkit, allowing you to get on with the job with less stress and worry.

Who should consider it?

Contract works insurance is recommended for small, medium and large commercial, industrial and domestic builders, sub-contractors and owner-builders.

Most owner builders take out contract works insurance for a specific contract, while professional builders generally choose an annual policy that covers multiple contracts.

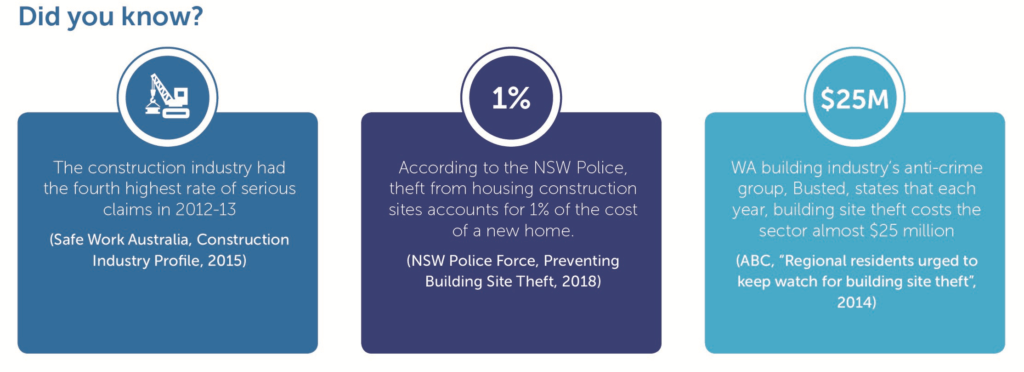

“There have been significant reduction in the numbers and rates of injuries and fatalities in this industry over the last ten years or more. Nevertheless, the construction industry remains a high risk industry.” Safe Work Australia, 2015

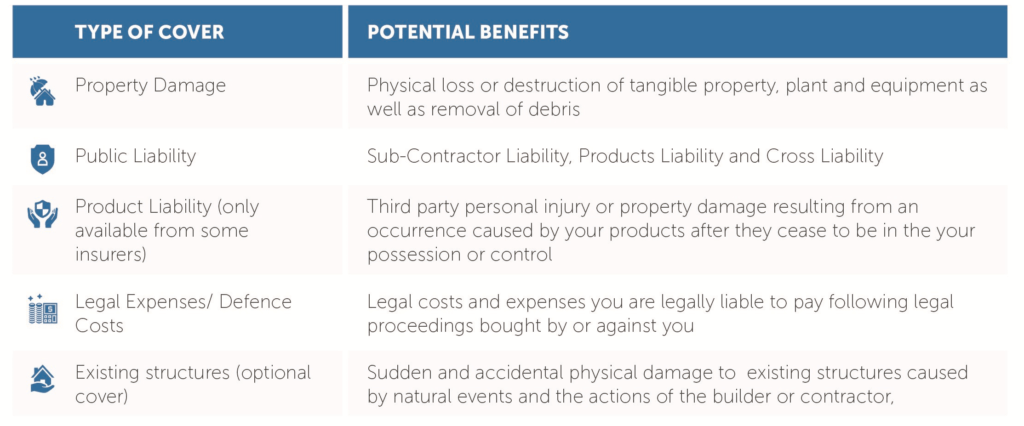

What can it cover?

Contract works insurance can cover the building which is under construction, whether it’s a kit home, straw bale or mud brick home, or multi story apartment or commercial buildings. It can also cover the equipment used in construction, as well as public liability risk.

Depending on your policy, contract works insurance can cover you against:

What usually isn’t covered?

Exclusions, the excess you need to pay and limits of liability can vary greatly depending on your insurer. Policies generally won’t include cover for:

- Loss after work has ceased for more than the number of days specified in the policy

- Consequential loss

- Cost of rectifying or correcting defective workmanship

- Work underground or in water unless specifically agreed by the insurer

Case Study

After working for other construction company owners all his working life, Craig starts his own small earthmoving firm. In the first couple of years, he borrows money and invests much of his income back into the business, buying the latest equipment and a work vehicle.

After starting work on a new construction at a new site, he leaves his tools and equipment locked in a garage on the site overnight. But that night, thieves break into the garage and steal Craig’s tools, worth $25,000.

Craig contacts his insurance broker who helps him put in a claim. He’s quickly reimbursed for his loss, so he isn’t out of pocket and can keep his business running.

Important note

This information is provided to assist you in understanding the terms, implications and common considerations in contract work insurance. It does not constitute advice, and is not complete, so please discuss the full details with your Steadfast insurance broker.